Much of the news on Friday’s jobs report was focused on whether or not the low unemployment rate (5.3 percent) and relatively strong payroll number (215,000) will compel the Federal Reserve Board to decide to raise short-term interest rates at its September meeting. Such a move would signal confidence in the health of the U.S. economy, and that the Fed believes that it has done enough to restore economic well-being for most Americans.

Yet, digging deeper than these top-line measures, one easily finds points of vulnerability, suggesting that the Fed should stay the course and postpone any interest-rate increase until there’s been more broad-based improvement in the labor market.

First, wage growth remains stagnant. According to Friday’s report, nominal average hourly earnings for private-sector workers increased by 5 cents from June to July, or by just 2.1 percent over the year. This is in line with the pace of growth throughout the recovery and well below the recommended rate of 3.5 to 4 percent.

Another clear sign that the Fed should hold off is the continued high level of long-term unemployment, or joblessness lasting for longer than six months. The number of long-term unemployed edged up to about 2.2 million people in July, or 27 percent of all jobless. This latter measure remains higher than any peak recorded prior to the Great Recession. The average duration of unemployment—which reached a record of almost 41 weeks in 2010—is down by about four weeks over the last year, to about 28 weeks; however, it, too, remains higher than any average duration recorded prior to this recession.

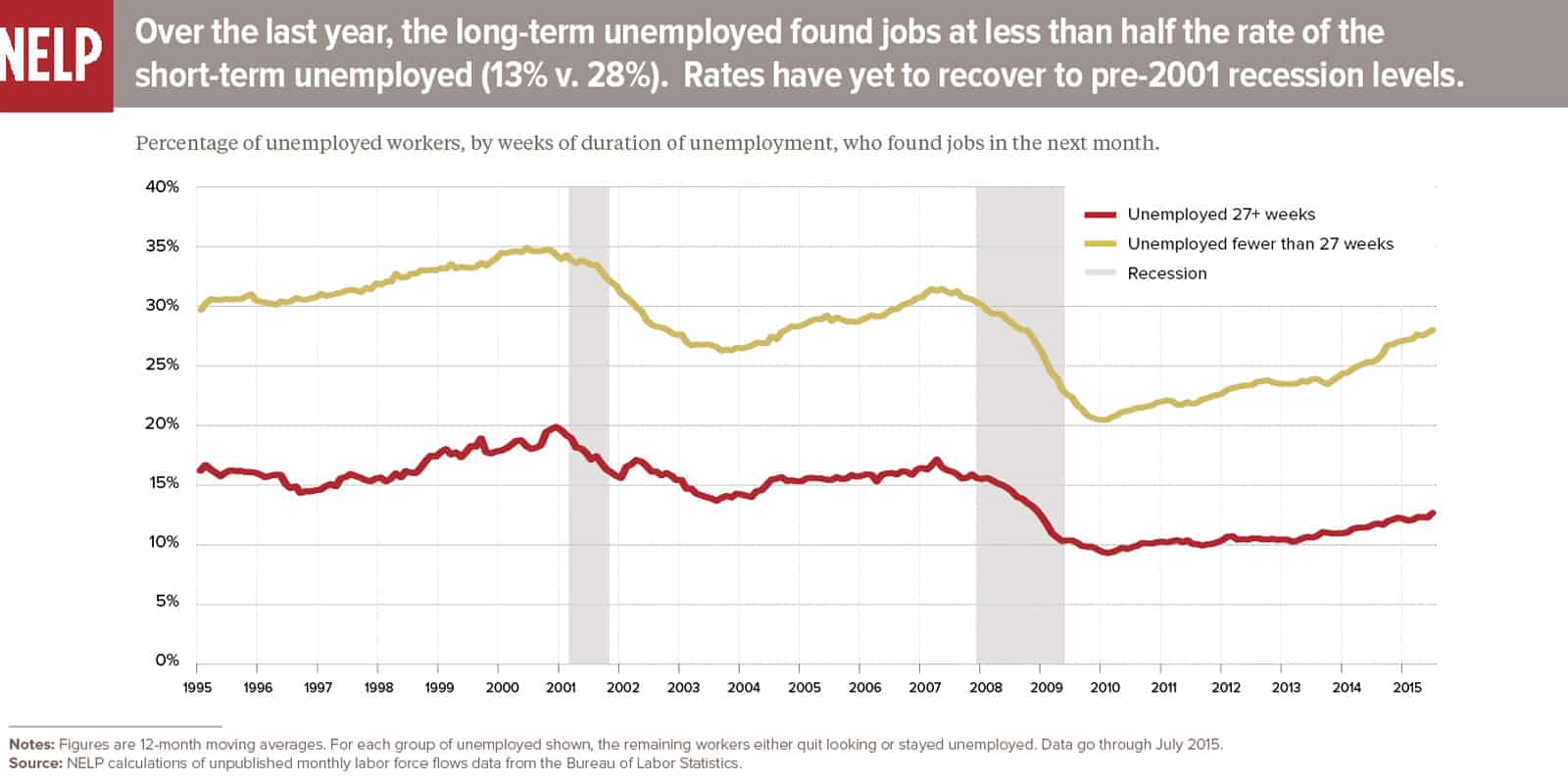

Another useful indicator of the difficulties the long-term unemployed face in the job market can be found in an unpublished data series on labor force flows from the Bureau of Labor Statistics. These data show the shares of unemployed workers, by their weeks of duration of unemployment, who from one month to the next either find jobs, remain out of work, or quit looking and drop out of the labor force.

The first figure shows the percentage of the unemployed, by their weeks of duration of unemployment (either fewer than 27 weeks, or 27 weeks or longer), who found jobs. Most obviously, the long-term unemployed find jobs at a much lower rate than workers unemployed for shorter durations. Over the last year, just 13 percent of the long-term unemployed found jobs compared to 28 percent of workers unemployed for shorter durations. More troubling, job-finding rates for both groups have yet to recover to pre-2001 recession levels: in the year ending March 2001, 19 percent of the long-term unemployed and 35 percent of the short-term unemployed found jobs.

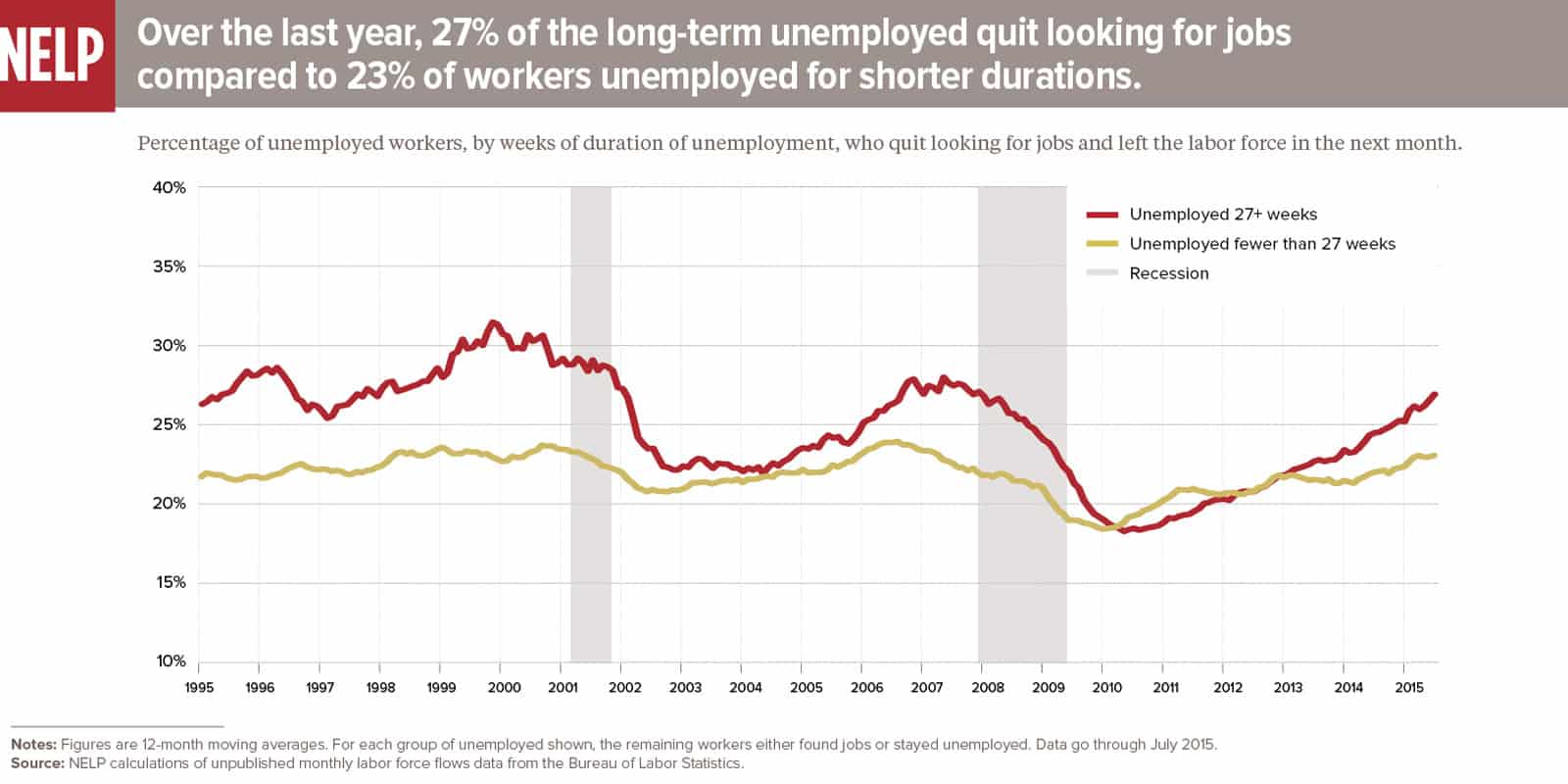

The second figure shows the percentage of the unemployed who quit looking for work and dropped out of the labor force. We can’t be sure from these data that all unemployed who leave the labor force do so because they’re discouraged by weak job opportunities; they may also decide to enroll in school or training, for example. However, the fact that labor force exit rates tend to be higher for people out of work for longer suggests that low confidence in re-employment prospects may play a significant role for many.

Over the last year, about 27 percent of the long-term unemployed left the labor force, compared to 23 percent of workers unemployed for shorter durations. Looking at the two figures together, one also sees that, consistent with earlier patterns, the long-term unemployed found jobs at less than half the rate that they quit looking and left the labor force (13 percent in the first figure versus 27 percent in the second figure; the remaining, largest share, not shown, stayed unemployed); it’s always the case that a higher share of the short-term unemployed find jobs than drop out.

The rate at which the long-term unemployed leave the labor force is usually greater than for the short-term unemployed, with the exception of the period after the Great Recession (notice the lines intersecting). This is likely tied to the availability of a record number of weeks of federal unemployment insurance (UI) benefits for workers who exhausted their regular state benefits (usually after 26 weeks), with the greatest possible durations occurring from roughly late-2009 until late-2012. In general, the availability of federal UI benefits probably helps to explain why exit rates for the short- and long-term unemployed dipped relatively low in 2002 and 2003 and in 2010 and 2011 (after the 2001 recession, federal emergency extensions began in March 2002 and lasted for roughly two years). During these times of very high long-term unemployment, many jobless workers waited longer than usual before they eventually stopped looking for work, in part because it was a condition of their continued eligibility for UI benefits.

Now just over six years into the official recovery, exit rates are returning to their historical norms, with the rate rising more for the long-term unemployed. Even though these patterns aren’t unusual, it’s still troubling that unemployment lasting for longer than six months means that you’re always going to be more likely to leave the labor force than find a new job, whereas the opposite is true for shorter unemployment durations. At the same time, the fact that job-finding rates, especially for the long-term unemployed, are still so depressed by historical standards means there’s still room for growth in the economy.

Related to

About the Author

Claire McKenna

Senior Policy Analyst, National Employment Law Project